Billion-dollar losses, soaring debt, and sharply negative margins. Criticism of the AP Funds’ green investments is growing after new revelations about loss-heavy ventures in both district heating and wind power—while earlier investments in Northvolt have already cost pension savers billions.

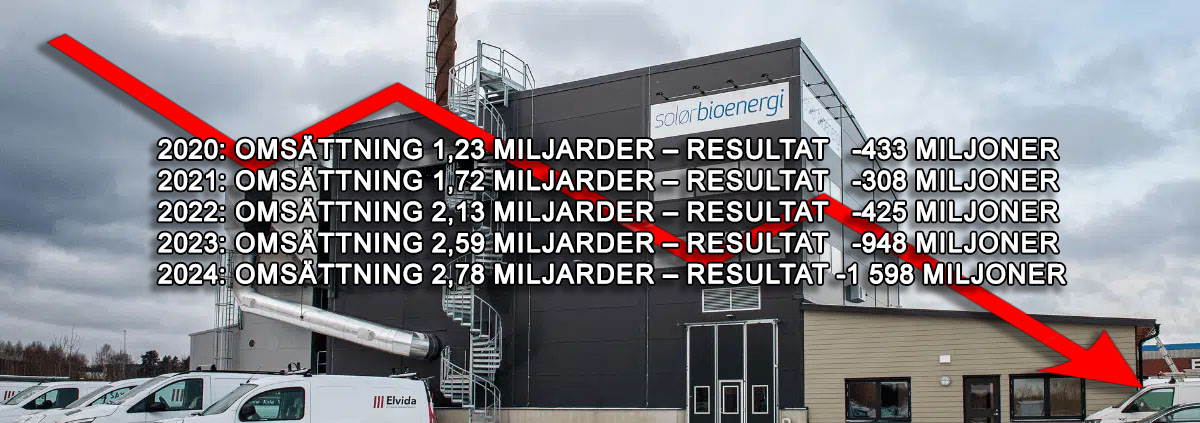

In a column for Affärsvärlden, the magazine’s columnist Christian Sandström delivers sharp criticism of the AP Funds’ investment in the district heating company Solör Bioenergi, where pension capital via Polhem Infra owns 40 percent.

The company has grown rapidly—but at a high cost. Revenue has more than doubled between 2020 and 2024, while losses have risen sharply.

At the same time, debts have nearly tripled—from SEK 7.4 billion to just over SEK 21 billion. Sandström describes this development as a “green-black hole” and questions how many such investments the pension system can withstand.

Despite the company raising its prices and being criticized by both the Swedish Competition Authority and the Energy Markets Inspectorate, losses continue to grow. Critics point out that the business model—buying up many small district heating networks—risks creating a structure that is difficult to oversee and cost-driving.

“Death Spiral” in District Heating

According to an opinion piece in Affärsvärlden by docent Mats Nilsson, more fundamental structural challenges lie behind the problems. He describes district heating as a classic network monopoly with high fixed costs—but where demand is no longer growing.

Production has remained steady at around 50 TWh per year for over a decade. At the same time, energy efficiency is reducing demand, heat pumps are taking market share, and volume per customer is dropping.

ALSO READ: Expert slams AP Funds’ wind power investments—bleeding pension money

Meanwhile, the sector faces massive reinvestments. A large part of the infrastructure is over 50 years old, with the cost of replacing old pipes estimated at around SEK 70 billion.

Nilsson argues that this creates a classic “death spiral”—decreasing customer base + increasing costs → higher prices → further decreasing demand. He contends that policymakers should begin to plan for a controlled dismantling rather than expansion—while the state may need to take greater responsibility for financing and price regulation.

Wind Power Investment with Minus 329 Percent

The problems are not limited to district heating. In another column, Christian Sandström highlights the wind power project Skaftåsen, where the AP3 and AP4 pension funds, via Polhem Infra, own 23 percent.

The figures for 2024 are striking: Revenue: SEK 76 million. Result: -SEK 249 million. Loss margin: -329 percent. The previous year was somewhat better, but still heavily in the red.

Sandström notes that wind power in Sweden has long had returns ranging from weak to none to negative. This is especially true in Norrland, where average margins have hovered around -63 percent during 2017–2024. In Skaftåsen’s case, the situation was further worsened by technical problems that knocked turbines out of operation.

Criticism also points to an asymmetry: while the pension funds bear the losses, the project developer has been able to make substantial profits. When the project was sold, it was calculated to provide about SEK 210 million in positive results for the developer.

Sandström summarizes the criticism in sharp words: “On one side stand virtue-signaling civil servants … on the other side a listed company ready to squeeze out as many kronor as possible.”

Northvolt – Billion-Dollar Loss After Political Decision

The perhaps most high-profile deal concerns battery manufacturer Northvolt. The AP Funds invested a total of about SEK 5.8–6 billion in the company—money that was lost when the company plunged into deep crisis and went bankrupt.

ALSO READ: The AP Funds’ Northvolt experiment has cost pension savers billions

The investment was made possible by political maneuvering. Legislative changes between 2018–2020 opened up for “sustainable” investments. The ban on investments in unlisted companies was removed. The AP Funds created their own venture capital/shell company to carry out the investment.

ALSO READ: Politicians changed the law—invested pension money in Northvolt

The initiative was at the time described as strategically important for both the climate and Swedish industry. Dissenting voices were present but dismissed. In hindsight, the critics have been proven right, and their ranks have grown, not least regarding the risk level of the investment, lack of transparency in decision-making, and the fact that documentation and emails were deleted or classified.

Recurring Pattern

Overall, a recurring pattern emerges in the criticism: political pressure for “green” investments, capital-intensive projects with uncertain profitability, high losses or weak returns, and risks eventually borne by pension savers.

Polhem Infra, which was created to combine sustainability with returns, is in several contexts highlighted as an example where the outcome so far has, to put it mildly, not lived up to ambitions and promises.

Growing Questions of Responsibility

The recurring question—not least in Sandström’s columns—is how many such investments the pension system can sustain. Meanwhile, Mats Nilsson’s analysis shows that some of the problems are not only about individual investments but about structural challenges in entire sectors.

This leaves pension savers caught between climate policy ambitions and the need for stable returns, with several outcomes so far having proven costly.